Advertisement

Advertisement

Hang Seng, Nikkei 225, and ASX 200 Rally as Fed’s Rate Cut Fuels Optimism Across Asia

By:

Key Points:

- Fed surprises with a 50-basis point rate cut, boosting investor confidence in US and Asian equity markets.

- Hang Seng rallies 1.18% as rate-sensitive stocks surge, supported by Hong Kong's response to the Fed's rate cut.

- ASX 200 hits a new intraday high, driven by gains in mining and banking stocks.

In this article:

US Equity Markets See Late Pullback

On Wednesday, September 18, the US equity markets ended the session in negative territory. The Dow declined by 0.25%, while the Nasdaq Composite Index and the S&P 500 saw losses of 0.31% and 0.29%, respectively.

The US indices climbed to session highs in response to the Fed interest rate decision and projections before falling into the red.

Fed’s 50-Basis Point Rate Cut Surprises the Markets

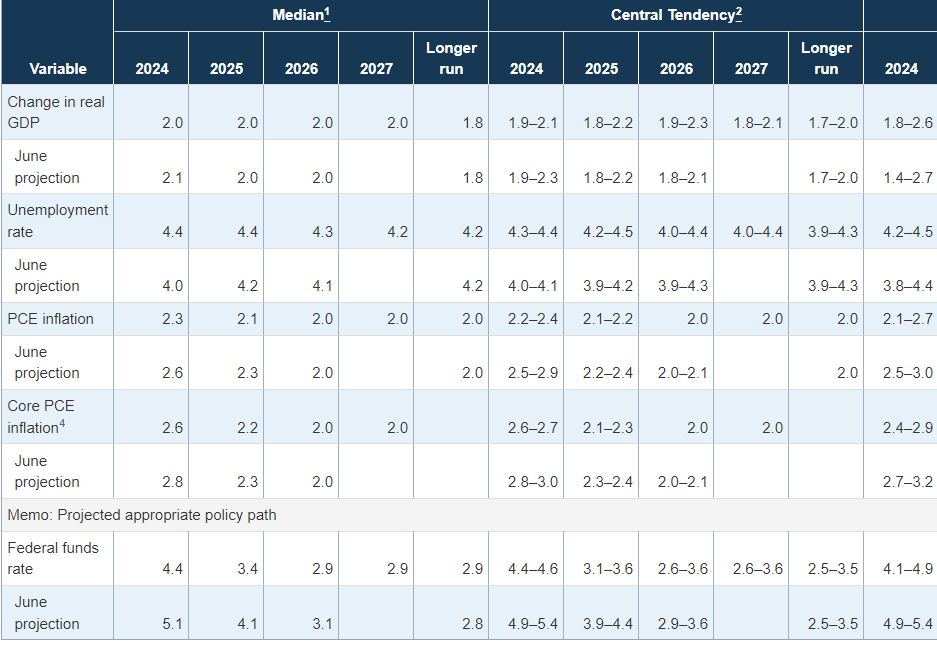

On Wednesday, the Fed cut interest rates by 50 basis points, surpassing expectations of a 25-basis point interest rate cut. The FOMC Economic Projections supported bets on a soft landing for the US economy, which drove demand for riskier assets. The Fed also projected a more dovish future Fed rate path.

Growth forecasts of 2.0% from 2024 to 2026 and expectations of more aggressive rate cuts set a positive tone for Thursday’s Asian session.

Aussie Labor Market Data Signal Stable Conditions

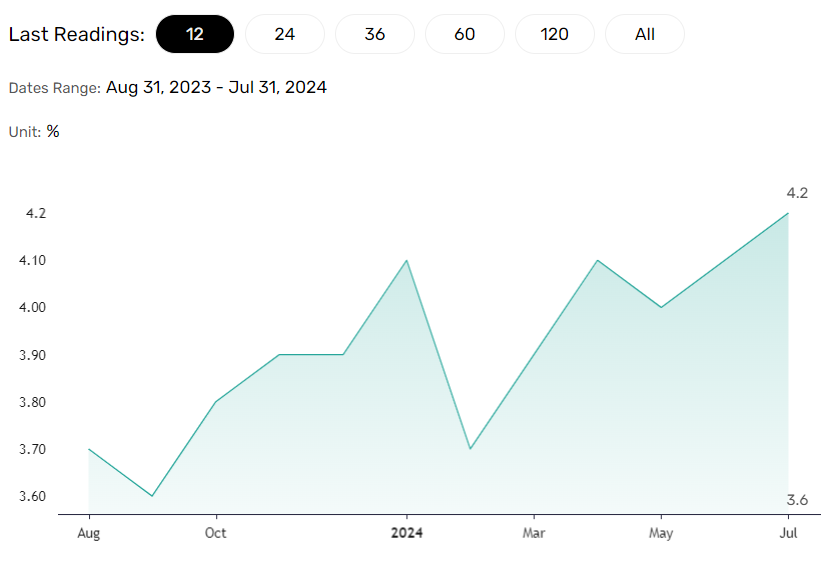

On Thursday, September 19, Australian labor market data indicated continued stability. The unemployment rate held steady at 4.2% in August, with part-time employment rising by 50.6k, offsetting a 3.1k fall in full-time employment.

Steady labor market conditions could temper investor expectations of a Q4 2024 RBA rate cut. However, the data could support wage growth, consumer spending, and overall Australian economic strength.

Expert Views on the Australian Labor Market

Kate Lamb, ABS Head of Labor Statistics, commented on the labor market figures, stating,

“The high employment-to-population ratio and participation rate shows that there are still large numbers of people entering the labour force and finding work, as employers continue to look to fill a more than usual number of job vacancies.“

Hang Seng Index and Mainland China Markets React to Fed’s Move

On Thursday, the Hang Seng Index rallied 1.18% as investors reacted to the Fed rate cut and projections. The Hong Kong Monetary Authority (HKMA) mirrored the Fed’s overnight 50-basis point rate cut, driving demand for rate-sensitive stocks.

The Hang Seng Mainland Properties Index surged 4.77% on lower borrowing costs that could bolster the sector. Tech stocks also benefitted from the rate cuts, with the Hang Seng Tech Index (HSTECH) advancing by 2.27%. Alibaba (9988) and Baidu (9888) rose 2.47% and 2.65%, respectively, with Tencent (0700) advancing by 1.45%.

The mainland China markets also advanced, with The CSI 300 and the Shanghai Composite seeing gains of 1.04% and 0.81%, respectively.

Nikkei Index Rises Alongside the USD/JPY

The Nikkei Index was 0.49% higher on Thursday morning. Easing fears of a hard US economic landing drove buyer demand for the USD/JPY and Nikkei-listed export stocks.

Nissan Motor Corp. (7201) jumped by 4.18%, while Fast Retailing Co. Ltd. (9983) rallied by 3.06%.

The tech sector benefited from the Fed’s rate cut. Tokyo Electron (8035) and Softbank Group Corp. (9984) advanced by 1.80% and 2.84%, respectively.

ASX 200 Strikes Another Intraday High

The ASX 200 Index gained 0.25% on Thursday morning after reaching a new intraday high of 8,187. Banking and mining stocks contributed to the morning gains.

Rio Tinto Ltd. (RIO) rallied 2.55%, while BHP Group Ltd. (BHP) and Fortescue Metals Group Ltd. (FMG) saw gains of 1.84% and 1.38%, respectively. Iron ore prices were higher on Thursday, boosting demand for the mining giants.

ANZ Group Holdings Ltd. (ANZ) and Westpac Banking Corp. (WBC) advanced by 1.25% and 0.93%, respectively. The Fed’s 50-basis point rate cut drove demand for Australian banks, well known for high dividend yields.

With the focus on the Fed rate decision and projections, investors should remain alert and closely monitor news wires, real-time data, and expert commentary to adjust trading strategies accordingly. Stay informed with our latest news and analysis to manage positions across the Asian equity markets.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement